After a torrid two-year spike in sales and prices in 2020 and 2021, the housing market in the New York metropolitan region downshifted last quarter. Sales fell dramatically from the previous year’s all-time highs, hampered by a sharp rise in interest rates, “sticker shock” at home prices, and a lack of sellable inventory. But even with the decrease in number of homes sold, prices continued to appreciate, reaching new all-time-highs throughout the region.

When we analyze our regional housing market, we generally make comparisons to the prior year, because year-on-year changes are usually pretty reliable indicators. But when the market has been as volatile as our housing market has been over the past few years, we think it’s important to take a bit of a longer view of what’s going on. So in our overview, we’re going to make comparisons not just to last year’s fourth quarter and the full 2021 prior calendar year, but also to the 2019 calendar year. Why? Because 2019 was the last pre-Covid year, with a relatively “normal” housing market that we think provides a good model for where the market is going in 2023.

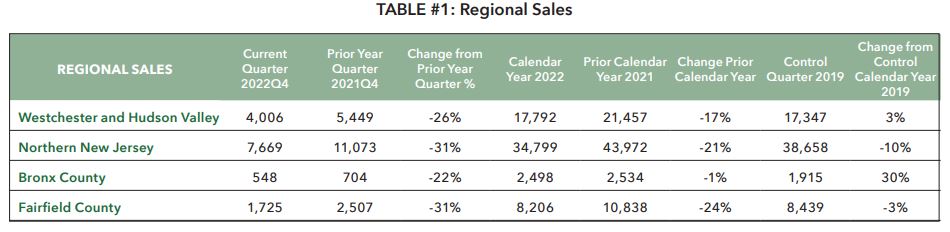

Sales fell dramatically from their all-time-highs of 2021, but remained consistent with their pre-COVID-Boom levels. The amount of homes sold fell sharply over the past year, dropping about 36% in Rockland County. But the story is more mixed if you look at the transaction levels in our 2019 control year. When we look at the 2019 sales, we see that closings are basically similar to what we saw before the COVID Boom, which we considered a strong year.

The central question is whether this downward sales trajectory will continue through 2023, or whether we’ll see stabilization at those pre-COVID “normal” market levels. The bearish argument is that prices might have reached a height that scares away too many buyers, interest rates are still in the mid-6% range, and that inventory levels are still so low that we don’t have enough “fuel for the fire” to keep the market going. According to that view, we’ll continue to see sales fall another 10-15% in 2023, which would bring transactions down to 2014-15 levels.

The more bullish argument is that sales could level out at their current levels, for a couple of reasons: first, buyers might come back into the market with prices flattening out. Second, buyers might become more accustomed to the higher interest rates (and might enjoy rates coming back a bit this spring); and third, homeowners might build confidence that they can put their home on the market without worrying about having nothing to buy, which would help our inventory troubles. More importantly, recent economic news has been positive, with unemployment at all-time lows, inflation going down, and the economy continuing to grow. People who have jobs tend to buy homes.

So which is it? One clue to the future comes from the “Pending Sales,” which are deals that have gone into contract during the time period (either the quarter or the year). Pending sales are down dramatically from last year’s highs, but are in the ballpark for what we saw in 2019, before the COVID Boom.

Pending sales are our best predictor of future closed sales, so we think that transactions will probably stay close to but slightly below 2019 levels at least through the Spring.

The best bullish case, though, has to do with the lack of available inventory: we still don’t have enough available homes on the market, which should continue to prop prices up even if buyer demand slacks off. Inventory came up a bit in the fourth quarter, but still remains near historic lows. Inventory levels are currently at 1.7 months for single-family homes in Rockland County. This number is calculated by dividing the amount of homes we have for sale by the average amount of buyers that go to contract each month. (6 months of inventory is considered a neutral market, with more than 6 months favoring buyers.) 1.7 months is incredibly low from historical standards. And that’s why we are relatively bullish on prices. It’s just basic economics. Even if buyer demand falls, this kind of restricted supply should prop prices up, and might even continue to drive appreciation throughout 2023.

As you can see, we are relatively bullish on the future of the market. Basically, we think that the market is returning to a pre-COVID state and are projecting that 2023 sales will track near 2018-19 levels, but that prices will stabilize at current levels that are about between 25% and 40% higher than they were just three years ago. We know that many of our clients, and even our colleagues, are anxious about the near future of the housing market. Much of that anxiety stems from the highly-charged media coverage we’ve seen over the past six months, which has amplified vivid narratives about (1) rising interest rates, (2) a dramatic sales decline, and even (3) industry layoffs by large public real estate and mortgage companies. But we believe that this bearish case is overstated, and that these narratives are misleading. Here’s why:

1. Interest Rates. Yes, interest rates have gone up, and that’s a real problem for the market. But we might have already seen rates top out, and many buyers have adjusted to the new financing realities by opting for adjustable rate mortgages and putting more money down. Interest rates have certainly hampered the growth of the market, but they haven’t been the dagger-in-the-heart that many media accounts seem to think.

2. Sales Decreases. When the media writes about sales figures, they generally (and naturally) make comparisons to 2021. But 2021 was just about the strongest real estate market in history! It’s not a fair comparison. Yes, as we’ve shown here, sales are sharply down from their all-time-highs, but they’re comparable to the “normal” pre-COVID market, which was not a market that sparked any real anxiety. If we track 2018-19 levels for the rest of the year, the market will be just fine.

3. Industry Layoffs. The media, particularly industry media, has been breathlessly reporting about layoffs in large, public real estate companies. Yes, those companies have been laying people off, but that has less to do with the housing market than the stock market – those companies have all seen dramatic declines in their share price, which has forced them into those layoffs. Moreover, many of the real estate companies laying people off are reliant on mortgages, particularly refinances, for their profitability, and the refi business has cratered this year. Finally, we all know that the media (particularly social media) loves a scary story, and narratives involving the “collapse of the housing market!” make for good engagement and eyeballs. That’s one of the reasons we’ve been putting out this Quarterly Market Report four times a year, because we think it’s important for our clients, colleagues, and community get an objective, facts-based analysis of the housing market. Accordingly, we hope that you found this Report helpful, and encourage you to reach out if you have any questions.

Sorry, the comment form is closed at this time.