The housing market in the Hudson Valley continues to experience dramatic price appreciation in the first quarter of 2022, but for the first time since the beginning of the Pandemic we started to see a slowing of sales activity. That decline in both closed and pending sales was mostly due to a lack of inventory but we also saw a significant surge in interest rates, which might have a longer-term impact in cooling down the market.

The Big Story: Rates Finally Go Up

The biggest story of the first quarter was a long-awaited rise in interest rates. It felt like we had been talking about “historically-low” interest rates for many years as rates went under 3% during the Pandemic Market. Year after year, we kept expecting that they might start to go up, only to see them continually go down.

Well, all that ended in the first quarter of 2022, with interest rates surging, largely because of a red-hot economy driving a spike in inflation. The average interest rate throughout 2021 was 2.96%, but by the end of the first quarter, rates had risen up to over 4.5%, with legitimate concerns that they might continue to go up throughout the year. This increase might be giving some buyers “sticker shock” but from a longer-term perspective, today’s rates are comparable to where they have been for most of the 2010s, and are significantly lower than the last seller’s market of the 2000s.

All that said, rising interest rates can obviously have a significant impact in the housing market. In the short-term, they tend to drive some new activity, as buyers rush to get into contract and secure a rate commitment before those rates continue to go up, and sellers put their homes on the market for fear that this seller’s market might be fading. Over the longer-term, though, higher rates could cool down what has been a torrid market, reducing the purchasing power of some buyers and pushing others right out of the market. For example, as rates go up from 3.0% to 4.5%, the borrowing power of a $1,000 monthly payment goes down by about $40,000, from almost $240,000 to just under $200,000.

What’s Going on in the Rockland County Real Estate Market?

We believe that the rising interest rates will not have much of an impact on sales or prices, at least through the summer. Why? Because inventory is just so low. Sales and Pending Contracts are down, but that’s largely because we can only sell what’s for sale – and we don’t have enough homes on the market. And we still have enormously strong buyer demand. Even with rates going up, buyers generally will adapt by opting for adjustable-rate mortgages or putting more down. So with demand high and inventory low, we believe that prices will continue to go up, at least through the end of the year. We doubt that we will continue to see double-digit appreciation for another year, but we simply see too much demand and too little supply to think prices will flatten out anytime soon.

Sales were down from last year, but largely because of the lack of inventory.

Regional single-family home sales fell for the second quarter in a row, which might signal a cooling of the torrid housing market of the last two years. But the overall picture was a little muddled, for a few reasons.

First, we are again measuring the quarterly sales figures against what might turn out to be the high-water transactional mark in the history of the region. That is, sales are down from last year’s first quarter, but they are up 20% from the Pandemic-impacted first quarter of 2020, and 27% from the pre-Pandemic 2019. So the fact that they’re off from that high-water mark doesn’t necessarily mean that this trajectory will continue throughout the year.

Second, the longer-term trend was fairly stable. If you look at single-family home sales for the rolling year, they were down just 1.4% from last year regionally.

New pending contracts cooled down after a torrid streak.

Another possible signal of a cooling market is the decline in pending contracts. Pending contracts were down almost 7% regionally for the quarter, and were mostly down across the board. Again, just like with closed sales, the picture was a little muddled, for some of the same reasons. We are measuring pending sales against all-time high baselines, so a decline doesn’t necessarily mean a slow market. It just might just mean that the market isn’t quite as hot as it was in 2021. After all, pending sales are up 22% from the Pandemic-impacted first quarter of 2020, and almost 19% from the pre-Pandemic first quarter of 2019. The numbers are high, they’re just not as high as their all-time records.

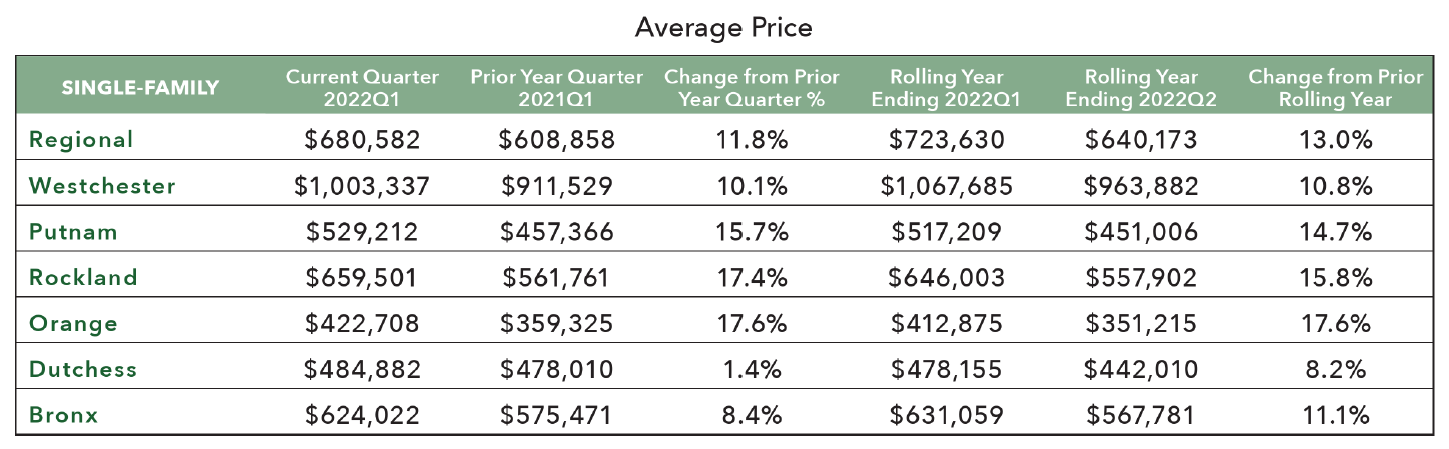

Prices continued to rise dramatically, reaching new historic highs.

Even with sales and pendings down, prices continued to reach new all-time highs throughout the region. Average sales prices in the region increased almost 12% for single-family homes from last year’s first quarter, and almost 17% for condos and coops. And for the rolling year, we saw double-digit appreciation in both property types, with average prices up 13% for single-family homes and 12.5% for condos and coops.

The question is whether those price increases will continue, now that the market seems to be cooling. But as we’ve discussed throughout this Report, the market is only “cooling” compared to the hottest market in the history of the region – that doesn’t mean the market isn’t still pretty “hot.”

The combination of high demand and low supply should continue to push prices up. Yes, interest rates are going up, but when rates go up, eager buyers simply adapt by opting for adjustable-rate mortgages or putting more money down so they can qualify for the loans they need.

Accordingly, we believe that we will not see another year of double-digit appreciation in 2022, but we do think that prices will continue to go up at least through the end of the year. Buyer demand is just too strong, and inventory is just too low, to suppress price increases. We still have a lot more buyers than sellers, and until that changes, prices will continue going up.

Sellers continue to hold negotiating leverage.

The seller’s market continued to give negotiating leverage to sellers over buyers, with ubiquitous bidding wars driving faster home sales at prices that are often higher than the asking price. In other words, the average home in our market right now sells for above the asking price. That’s unprecedented in this region.

We also look at the amount of time that a home is on the market, measured as the number of days between the listing date and closing date. Although it’s a bit imprecise, because it includes lots of “lawyer time” after a deal has been made, it does give us a general idea of how quickly buyers are snapping up homes for sale. Currently we’re seeing time on the market get as low as it’s ever been, at around two months to sell in Rockland.

Homes are selling quickly, and they’re selling near or higher than their asking price. We expect this will continue so long as low levels of inventory continue to force buyers to chase the homes that are available.

Sorry, the comment form is closed at this time.